What happens after the Bank gets my Money?

Understanding the Banking system and How Money Flows Through the Economy

When you deposit money into your checking account, do you ever wonder what happens to that money? Does it sit in a vault waiting for you to withdraw it? The reality might surprise you. Your bank only keeps a small fraction of your deposit on hand—typically around 10%, and lends out the rest. This is what is defined as “fractional reserve banking”, the system in the background that touches every dollar you earn, spend, and save. It's why your bank had the money to approve your small business loan, how you’re able to get a mortgage, and potentially why your 401(k) takes a nosedive during financial crises. While we might never think about this banking foundation, understanding it could be the difference between financial confusion and clarity in today's economy. Let's pull back the curtain on the system that makes the modern economy work...

Before we dive into the topic of the day, I’ll share a cool and random economic fact of the week. Let’s call these RBI’s (Random But Interesting). These facts will give us useful info, often with a picture or chart to make it clearer. The aim is to help us make smarter financial choices

Random But Interesting (RBI)

The Finance Hub is a reader-supported publication. To gain access to premium content and live webinar replays, consider becoming a paid subscriber

Now, back to our regular scheduled topic:

Money in our modern economy isn't what most people think. Every dollar in your pocket, every number in your bank account—it all began as debt. When you swiped your credit card for coffee this morning or took out a mortgage for your home, you didn't just borrow money—you helped create it. Our entire monetary system is built on lending, with banks turning your deposits into loans and loans into new deposits in an endless cycle. The Federal Reserve doesn't print most of our money supply; banks do, through this lending process. What seems counterintuitive is actually by design: our economy grows through expanding debt. The currency notes in your wallet are debts of the central bank to you, the numbers in your bank account is a debt that bank owes to you and your mortgage is a debt you owe back to the bank. This debt-based system accelerates growth and innovation but also explains why financial problems spread so quickly when lending freezes because the money fuels the economy stops flowing.

The Banking System Explained Simply

Imagine Sarah deposits $1,000 at First Community Bank. The bank keeps $100 (10%) as reserves and lends or invests the remaining $900. The recipients of the $900 lent or invested deposits it at their respective banks. These second banks keeps $90 (10% of $900) and lends out $810.

This process continues, creating a "money multiplier effect" where Sarah's initial $1,000 deposit can theoretically generate up to $10,000 in the economy through multiple rounds of lending and deposits. That’s why there is always way more debt than the physical currency available.

Fractional reserve banking serves as a powerful economic accelerator. By allowing banks to create money through the lending process, the system provides vital credit that fuels:

Business growth: Small businesses like your local coffee shop can secure loans to expand operations

Homeownership: Mortgage lending makes buying a home possible for millions of Americans

Education financing: Student loans help fund higher education and skills development

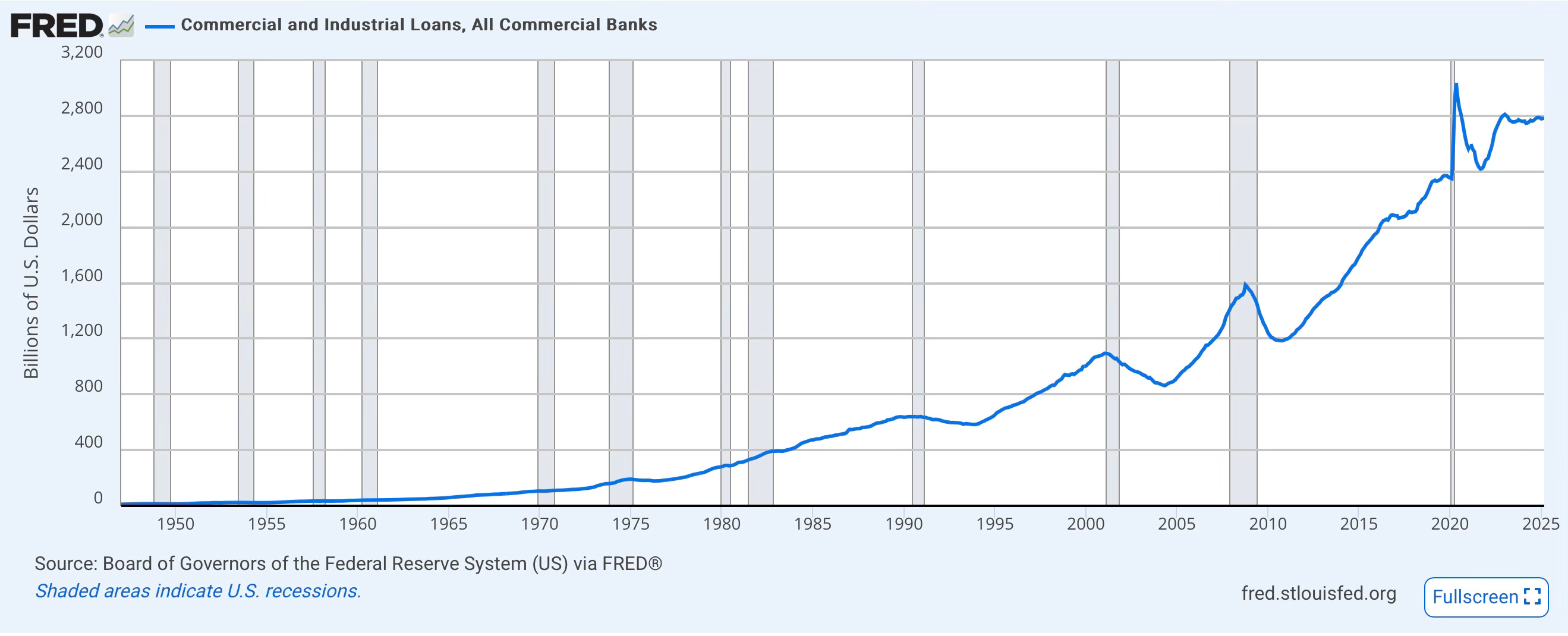

According to Federal Reserve data, U.S. commercial banks currently hold approximately $2.8 trillion in loans, supporting everything from auto purchases to business expansions. Without fractional reserve banking, enormous amounts of money would sit idle in bank vaults. Instead, this system puts capital to work, funding innovation and growth.

The interest income generated from loans and investments allows banks to offer services that many take for granted:

Free checking accounts

Convenient ATM networks

Mobile banking apps

Protection from fraud and theft

The fractional reserve system is an elegant when it works beautifully—until it doesn't. Since banks only keep a fraction of deposits on hand, they cannot withstand a situation where many customers demand their money simultaneously.

This vulnerability became painfully clear during the 2023 collapse of Silicon Valley Bank. When depositors learned of the bank's financial troubles, they withdrew $42 billion in a single day—far more than the bank had in reserves. Similar scenarios unfolded with Signature Bank and First Republic Bank, requiring regulatory intervention.

The interconnected nature of banking means problems can spread rapidly. During the 2008 financial crisis, what began as issues in the subprime mortgage market cascaded through the entire global financial system.

As described in the earlier example, you can see how bank funds can become so intertwined through complex financial instruments that the failure of Lehman Brothers threatened to bring down the entire system. This contagion effect required unprecedented government intervention, including the $700 billion Troubled Asset Relief Program (TARP).

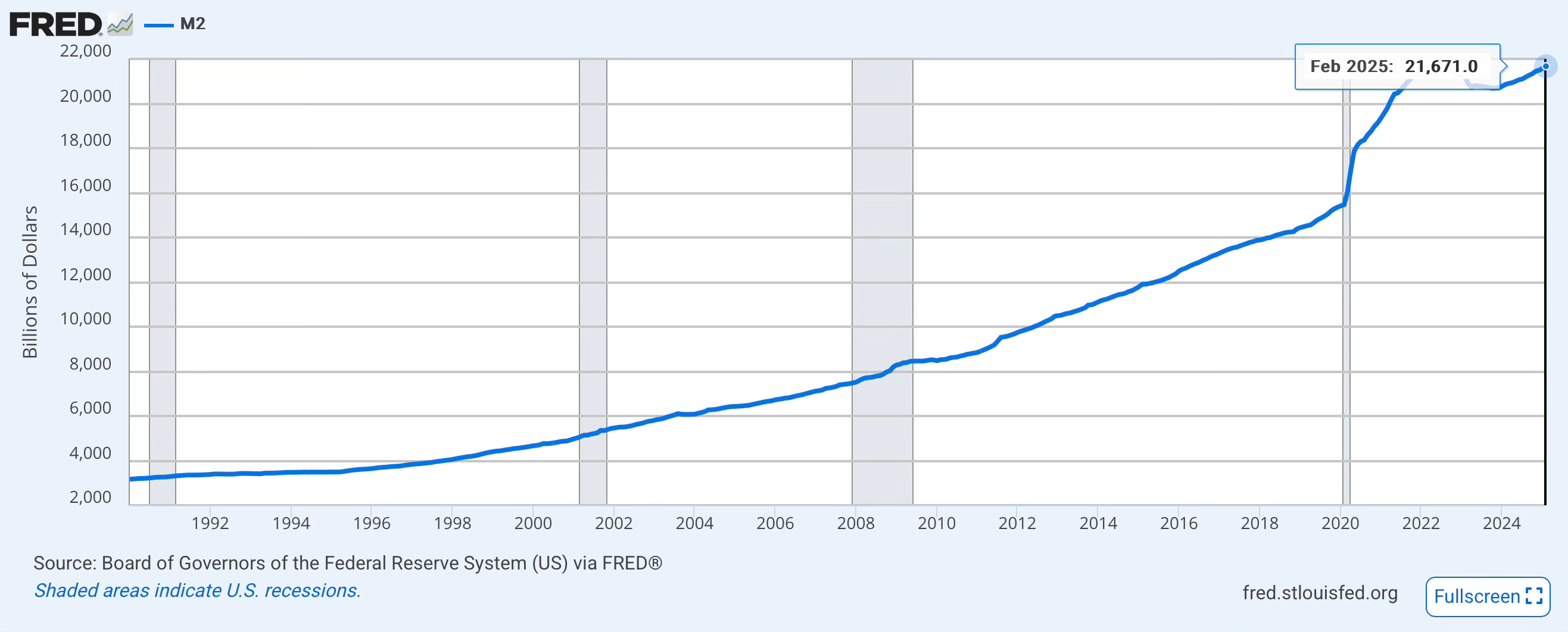

The money creation aspect of fractional reserve banking can contribute to inflation when economic output doesn't keep pace with the expanding money supply. During the post-COVID economic recovery, the money supply (M2) increased by nearly 40% between February 2020 and its peak in March 2022. This rapid expansion, while necessary during the crisis, contributed to the subsequent inflation surge we've experienced.

Given these risks, several safeguards exist to protect the fractional reserve system:

1. Deposit Insurance

The Federal Deposit Insurance Corporation (FDIC) insures deposits up to $250,000 per depositor, per bank. This insurance dramatically reduces the incentive for bank runs by reassuring depositors that their money is safe regardless of the bank's condition.

2. Central Bank as Lender of Last Resort

The Federal Reserve stands ready to provide emergency liquidity to solvent banks facing temporary shortages. During the 2008 financial and 2020 COVID crises, the Fed provided trillions of dollars in emergency loans to financial institutions.

3. Regulatory Oversight and Capital Requirements

Banks must maintain certain capital levels relative to their risk-weighted assets. The Basel III international banking regulations, implemented after the 2008 crisis, require large banks to hold capital equal to at least 8% of their risk-weighted assets.

Practical Implications for Everyday Banking

FDIC Insurance Limits: Ensure your deposits stay below the $250,000 insurance cap. If you have more than this amount, consider spreading it across multiple banks.

Bank Health Awareness: While you don't need to obsessively track your bank's financial statements, be aware of news regarding your financial institutions.

Emergency Fund Accessibility: Consider keeping a small portion of your emergency fund in cash. During a severe financial crisis, electronic payments and ATM networks could face disruptions.

For our Finance Hub members, we will cover some practical investment applications of this knowledge below:

Keep reading with a 7-day free trial

Subscribe to The Finance Hub to keep reading this post and get 7 days of free access to the full post archives.