The Two-Track Economy

The Policy contradiction that is quietly splitting the economy in two

Our government is running three policies at once that don’t necessarily agree with each other.

Fiscal policy (domestic government spending) wants growth. Trade policy (with other countries) is losing its legal footing. Monetary policy (from the central bank) is stuck holding rates in the middle, unable to fully address price stability or full employment. That contradiction does not affect everyone in the country and internationally evenly, but transmits through asset prices first. If you hold equities, real estate, or hard assets, you capture the upside of this environment. If you only rely on your wages and cash, you absorb the cost side: higher prices, a softening labor market, and no offsetting gains.

This is the direct output of our current economic environment. In this article, I will be explaining the mechanism, with the numbers behind each piece.

The inflation problem is not cooling on schedule

The inflation number in May was 4.2%, the largest 12-month increase since April 2023. At the same time, the labor market is losing momentum. June payrolls added 57,000 jobs against a 110,000 jobs forecast. A softening labor market normally argues for the Fed to cut rates.

The problem? Inflation running at nearly double the Fed’s target does not allow it to provide the lower rates.

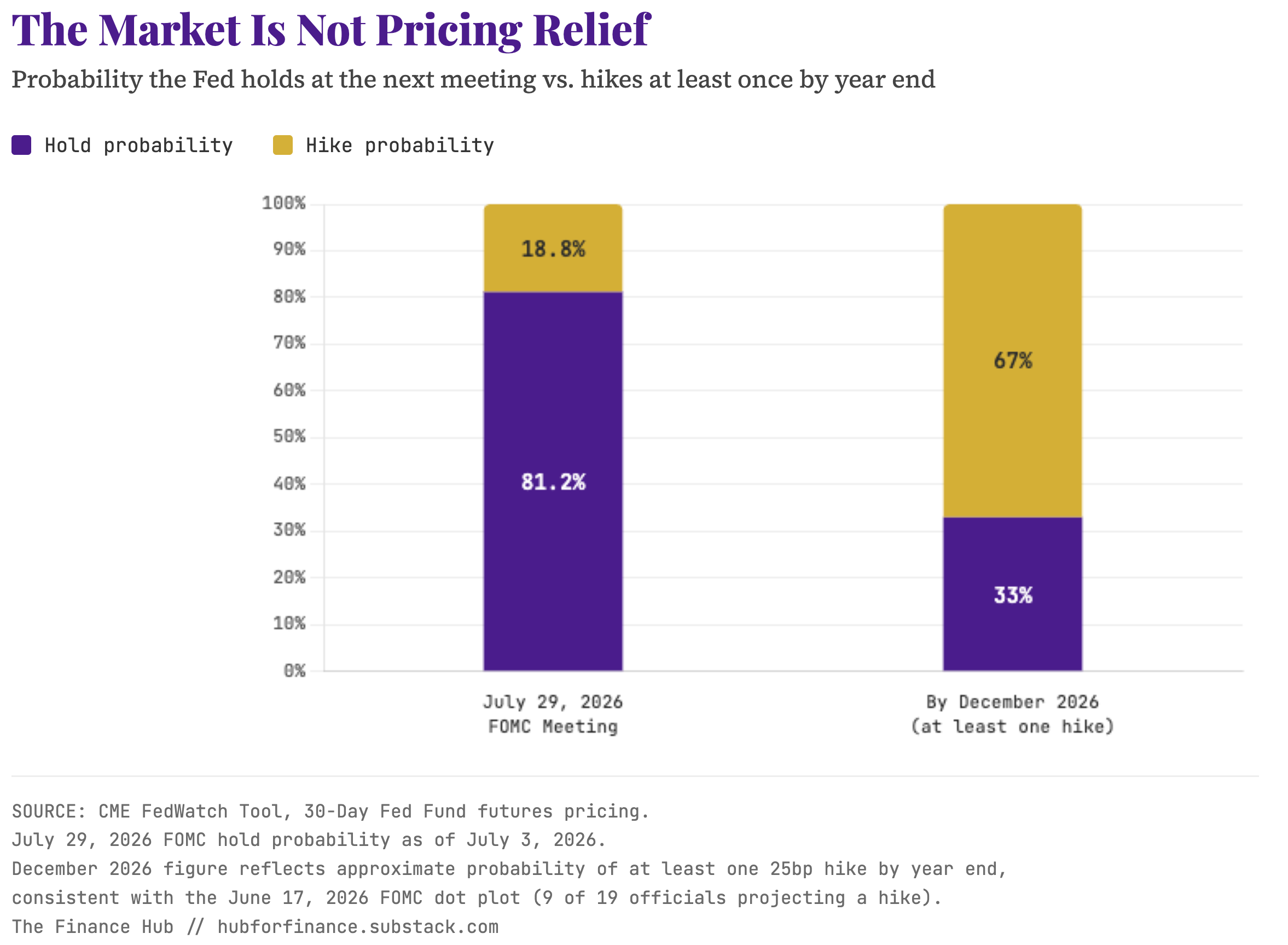

The Fed held its target rate at 3.50% to 3.75% on June 17, a unanimous 12-0 vote. The next FOMC (Federal Open Market Committee) meeting is July 28-29. As of July 3, CME FedWatch prices an 81.2% probability the Fed holds again at that meeting. But the committee’s own dot plot shows 9 of 19 officials projecting at least one hike by year-end, and CME FedWatch pricing implies roughly a two-thirds probability of at least one hike by December.

The market is not pricing relief. It is pricing a Fed that may need to tighten into a weakening jobs picture, because inflation will not let it do anything else.

Trade policy just lost a legal battle it has not finished fighting

On May 7, 2026, the Court of International Trade ruled that the administration exceeded its authority in imposing the Section 122 tariff surcharge in April last year. That ruling is under appeal.

At the same time, a new investigation targets 60 countries, including the European Union, for potential tariffs of 10% to 12.5% on forced labor grounds. This reopens a trade conflict with Europe that a prior agreement was supposed to have settled.

Any company that built its cost model around a stable tariff regime now has exposure on two fronts. The court could strike down the current surcharge on appeal. A new investigation could add fresh tariffs on a different set of trading partners. Neither outcome can be priced in with confidence till the outcome is resolved.

Fiscal policy is pulling in the opposite direction

Business investment rose more than 10% in the first quarter of 2026, driven by expenditure on equipment and R&D related to Artificial Intelligence development. This is a deliberate capex push. It is designed to maintain high growth.

Here is the contradiction. You cannot run a capex-driven growth agenda, a tariff regime that raises input costs, and a 2% inflation target at the same time without something giving. Full expensing incentives push more capital into equipment and business equity. They do not push capital into wages. The growth this policy generates shows up first on the balance sheets of whoever owns the business, not the paycheck of whoever operates the equipment.

Where the K shape comes from

Each of these three forces pushes asset owners and wage earners in different directions, which is very visible in the data.

Real average hourly earnings fell 0.7% year over year through May 2026. This means that workers are losing purchasing power in real terms, even as nominal wages rise.

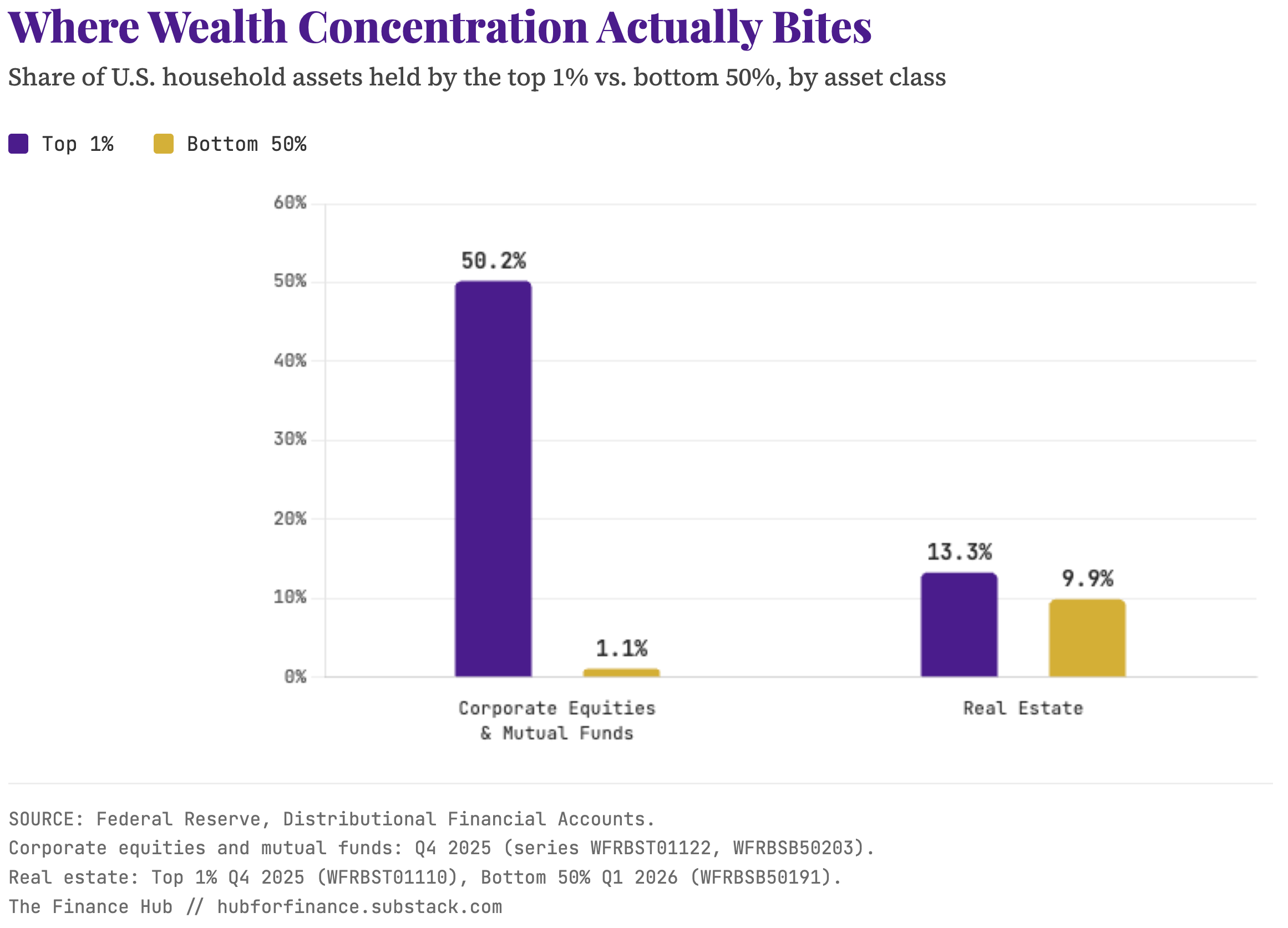

Compare that to asset ownership concentration. According to the Federal Reserve’s Distributional Financial Accounts, as of Q4 2025, the top 1% of households by wealth hold 50.2% of all corporate equities and mutual fund shares. The bottom 50% hold 1.1%. That is a 46-to-1 gap.

Real estate tells a different story. The top 1% hold 13.3% of real estate. The bottom 50% hold 9.9%. The gap here is real, but it is nowhere near as extreme as the equity gap.

This difference matters, and most people talking about the K-shaped economy miss it. A small group of wealthy people own most of the stocks. Real estate ownership is spread out more evenly. So if you’re starting to build wealth for the first time, a focus on the stock market might be a good bet since there is less competition than in real estate.

Why this matters for how you allocate capital

None of this requires a conspiracy. It is the mechanical result of who owns the assets that current fiscal and monetary policy are inflating.

Capex spending flows into equity earnings and business balance sheets. It does not flow directly into paychecks. Inflation running above wage growth erodes real income for anyone without an asset base to offset it. The Feds rate hold keeps financing costs elevated for renters and first-time buyers, while doing comparatively little to holders of existing fixed-rate mortgages or already-appreciating portfolios.

Right now, big companies get a tax break called “full expensing”. It lets them deduct the full cost of new equipment right away, instead of spreading it out over many years. This is a big reason companies are spending so much on equipment right now.

But this tax break isn’t just for big corporations. Small business owners can use it too. If you own a business, or own part of one, and you buy equipment, you can use this same tax break. This is a real, specific opportunity available today. It’s not just generic advice telling you to “buy assets.”