Live like the 1% (Part 1)

Bitcoin-Collateralized Loan Analysis

We’ve all heard the saying: the wealthy don’t spend their money, they borrow against their assets. It’s a well used strategy used to avoid triggering taxes, hedge against inflation, and stay fully invested to ride the wave of asset appreciation. Cash-out refinancing and Home Equity Lines Of Credit (HELOCs) are familiar strategies that regular people use to borrow against real estate. But what if you could do the same with your Bitcoin?

In this article, we explore a case study utilizing a bold financial strategy: taking out a loan backed by Bitcoin over five years, with 20–30% of the loan proceeds reinvested into Bitcoin itself. The goal? To use BTC’s potential long-term growth to offset interest payments or even generate profit without ever selling your original Bitcoin holdings. This is a modern twist on the classic “buy, borrow, die” approach. But with Bitcoin’s notorious volatility, does the math actually work out? In this multi-part series, we dive into historical data, model various growth scenarios, and compare this approach to traditional lending methods to find out whether this is a smart wealth-building tactic or a risky financial gamble. Now, I understand that today’s article might be a little dense, but if you can follow the logic, it could open up some new ideas on how to utilize this financial strategy. You can read this multiple times till it makes sense, and feel free to utilize the comment section to ask any questions you have.

Before we dive into the topic of the day, I’ll share a cool and random economic fact of the week. Let’s call these RBI’s (Random But Interesting). These facts will give us useful info, often with a picture or chart to make it clearer. The aim is to help us make smarter financial choices

Random But Interesting (RBI)

The Finance Hub is a reader-supported publication. To gain access to premium content and live webinar replays, consider becoming a paid subscriber

Now, back to our regular scheduled topic:

Before we dive into the case study, it’s important to note that one of the key reasons Bitcoin-backed loans are gaining momentum is their ability to provide fast, hassle-free access to liquidity, without the red tape of traditional lending. Unlike conventional loans, there’s no need for credit checks, income verification, lengthy application processes, or even monthly payments. Your Bitcoin acts as the collateral. If you have it, you're qualified. That simplicity means you can get approved and funded in a matter of hours, not weeks. For those who believe in holding their BTC long-term but need cash now, this model provides flexibility without forcing a sale. With the right conservative strategy, it is a smart option in both up and down markets.

A Bitcoin-backed loan process is designed to be simple and transparent. To get started, you deposit a minimum amount Bitcoin as collateral, and in return, you can borrow up to 50% of its value in USD. One of the standout features is the flexibility. There are no required monthly payments. Instead, the loan can be repaid at your own pace within the 12-month term, with the option to renew. However, if the value of Bitcoin drops and your Loan-to-Value (LTV) ratio hits 70%, you’ll receive a margin call to either add more collateral or repay part of the loan. If the LTV reaches 80%, the lender may automatically liquidate a portion of your collateral to bring the loan back into balance. This structure gives borrowers freedom and speed, while protecting both parties (lender and borrower) from downside risk.

Case Study: Bitcoin-Backed Loan Structure

A borrower considers taking a $250,000 loan using Bitcoin as collateral to cover living expenses. The proposed loan has a 12.4% annual interest rate (current interest rate for most Bitcoin-backed loans) and a 1-year term that can be renewed indefinitely. Instead of selling their Bitcoin, the borrower deposits it as collateral, allowing them to receive cash without triggering an immediate taxable sale of the Bitcoin. They plan to allocate 20–30% of the loan proceeds to buy additional Bitcoin, aiming for the asset’s appreciation to offset the interest costs. This strategy effectively leverages Bitcoin holdings: the borrower retains upside exposure (by holding and even increasing their BTC position) while obtaining liquidity. Below, we analyze the feasibility and risks of this approach including historical Bitcoin performance, tax treatment, margin call risks and compare it to traditional borrowing methods.

Historical 5-Year Bitcoin Performance

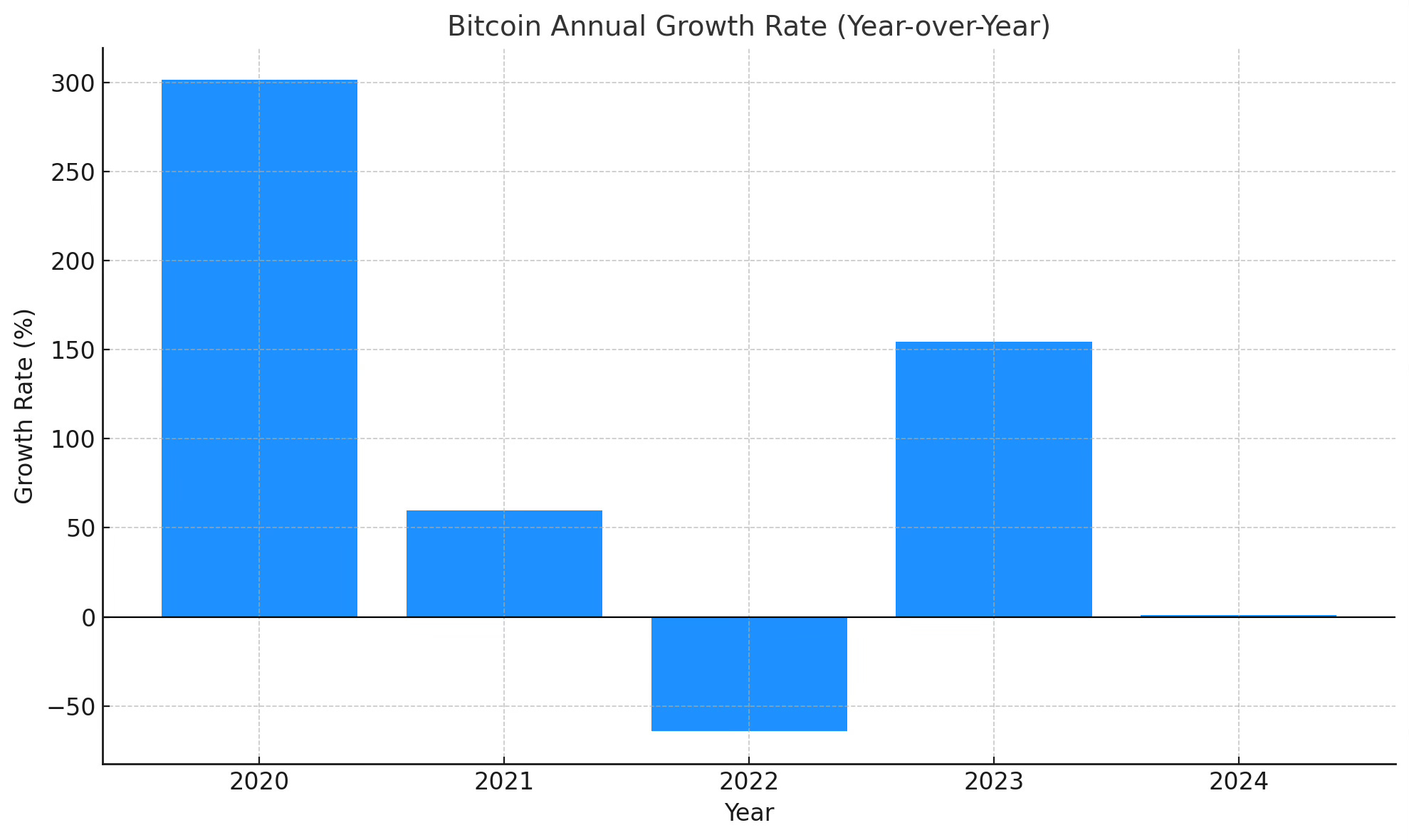

Bitcoin’s price history is notoriously volatile, but over most 5-year periods it has delivered explosive growth. In fact, Bitcoin has dramatically outperformed traditional assets over multi-year horizons. For example, over the five years leading up to late 2024, Bitcoin’s price rose about 1,283.6% (nearly a 13× increase). This equates to an average annual compound return well above 100%, far exceeding a 12.4% interest burden. Similarly, one chart noted Bitcoin’s 5-year compound annual growth rate (CAGR) at ~155% (per year) for a recent five-year span (an extraordinary growth rate that would handily cover interest cost). By contrast, traditional assets like stocks or gold gained roughly 85–97% total over the same 5-year period, highlighting Bitcoin’s historical outperformance.

Tax Implications of Bitcoin-Backed Loans (U.S.)

One motivation for Bitcoin-backed loans is tax efficiency. In the United States, loan proceeds are generally not treated as taxable income. Borrowing against Bitcoin allows the holder to raise cash without selling Bitcoin, thus deferring any capital gains that a sale would trigger. In this scenario, receiving $250k from a Bitcoin-backed loan does not create an immediate tax liability. The cash can be used for living expenses freely, since it’s a debt, not income. Also, the interest rate on the loan will typically be lower than the capital gains tax applied to a sale.

Importantly, depositing Bitcoin as collateral is not a taxable event in itself. The IRS considers cryptocurrency as property, and merely using it as loan collateral doesn’t count as disposing of it. This means the borrower avoids realizing capital gains on their Bitcoin at the time of the loan.

Interest payments on a personal Bitcoin-backed loan are generally not tax-deductible if the loan is used for personal expenses. Interest on personal debt (like using loan funds for living costs, tuition, etc.) is not deductible under U.S. tax law. Only in certain cases could the interest be deductible. For instance, if loan proceeds are used for investment purposes, the interest might count as investment interest expense (deductible up to investment income).

Collateral liquidation

A major tax pitfall is if the Bitcoin collateral is forcibly liquidated (sold) by the lender due to a price crash. If the lender sells some/all of the borrower’s Bitcoin to cover the loan, that is a taxable disposition . Even though the sale proceeds go to the lender (to repay debt) and not the borrower’s pocket, the borrower is still treated as having sold their property. They would owe capital gains tax (or realize a loss) based on the difference between the Bitcoin’s cost basis and the sale price. This could be especially painful if Bitcoin had appreciated significantly (triggering a large gain and tax bill) – or conversely, if it’s sold at a loss, the borrower realizes a capital loss (which might at least offset other gains). CoinLedger’s tax guide confirms that if your crypto collateral is liquidated to satisfy a loan, it’s “considered a disposal event” incurring tax liability.

Let’s wrap it up here for now. I hope you have found this information useful and it has provided you some insight into another way you can get liquidity from your digital assets. In the next part, we will go into the details of our case study, cover the risks of being margin called (losing out on your collateral), a comparison between Bitcoin backed loans and other sources of funding, analyze potential returns from implementing the strategy and also highlight companies we can utilize to implement this for ourselves. Please reach out if you have any questions.